Step-Up in Basis Appraisals: Eliminate Taxes

You Don’t Owe with an IRS-Compliant Valuation

Step-Up = Date of Death = Retrospective (they are the same)

A Step-Up in Basis appraisal is an IRS-compliant real estate valuation that resets the property’s tax basis,

helping eliminate unnecessary capital gains and estate tax exposure.

Whether you are just learning about Step-Up in Basis or already familiar with trust & estate matters, the terminology can be confusing.

Step-Up in Basis, Date of Death, and Retrospective appraisals all refer to the same IRS-compliant real estate valuation

which is the type of appraisal prepared as of a prior date, most commonly the date of death.

This IRS-compliant Step-Up in Basis appraisals helps you establish a new, higher taxable basis for your property

by documenting the fair market value as of your requested date. In markets like Silicon Valley, where real estate values

have increased on average by more than 5% annually, a properly supported Step-Up in Basis appraisal resets and thereby

eliminates unnecessary capital gains and estate tax exposure that results from the 'old' or original cost basis.

We guide trustees, executors, attorneys, & families through this process with prompt, high-quality appraisals—made simple and easy.

The outcome is a well-supported value that stands up to IRS scrutiny and provides confidence in tax reporting and fiduciary decision-making.

We routinely coordinate with attorneys and CPAs and are happy to work directly with you or with your professional advisors.

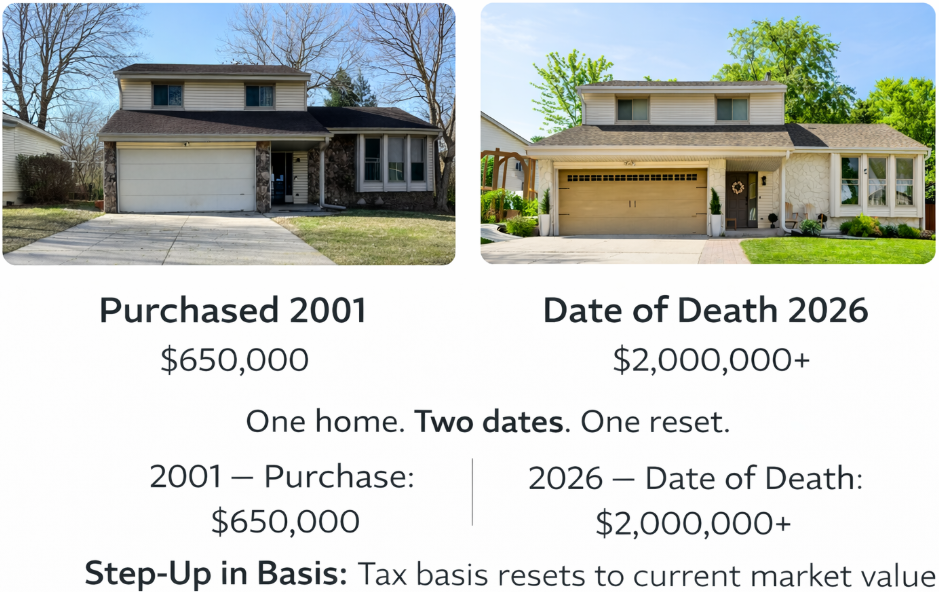

In the sample above, the Step-Up in Basis eliminated $1,350,000

of taxable exposure compared to the original cost basis.

Now 'What Do I Do With My Step-Up in Basis'?

Your Step-Up in Basis appraisal establishes the new tax basis for inherited real estate as of the applicable date (most commonly the date of death).

This value becomes the foundation used for tax reporting and future decision-making. Whether you are working with an attorney or CPA,

acting as a trustee or executor, or handling the process yourself, this appraisal is relied upon when:

-

Filing estate, inheritance, or informational tax returns

-

Calculating capital gains if the property is later sold

-

Establishing a defensible tax basis for recordkeeping and future use

-

Allocating assets among beneficiaries

-

Supporting reported values in the event of an IRS audit or inquiry

Because Step-Up in Basis appraisals directly affect tax exposure and fiduciary responsibility, they must be independent, well-supported,

and compliant with IRS and professional appraisal standards—regardless of whether the process is handled by professionals or independently.

With the 'New' Step Up in Basis What Are My Options?

A) Sell the Property Now or in the Near Future

Using the example above, if a property originally purchased for $650,000 receives a stepped-up value of $2,000,000 and is sold shortly thereafter

for approximately $2,000,000, the capital gains tax exposure is effectively eliminated. The stepped-up basis aligns with current market value,

so there is little or no taxable gain.

B) Retain the Property for Personal Use or as a Rental

If you or another family member retains the property—whether for 5, 10, or 15 years—the stepped-up basis remains in place. Using the same example,

if the property is later sold for $2,500,000, capital gains are calculated based on the stepped-up $2,000,000 basis, not the original purchase price.

Only the appreciation after the step-up date is subject to tax.

C) Hold the Property Until a Later Transfer

If the property is retained and later transferred again at death, a new Step-Up in Basis may apply at that time. In this scenario,

the next generation generally inherits the property based on its fair market value as of that later date—not the original purchase price decades earlier.

This is one of the primary reasons families obtain Step-Up in Basis appraisals: to avoid unnecessary tax exposure across generations.

Historical Appraisal Sample

Depending on the size of your property, the process takes approximately 30-40 minutes, prior to leaving we review with you to confirm details.

Afterwards, it takes 2-3 business days, and you will receive an email with a PDF that has 35-40 pages like the sample in the link below

(keep in mind the sample is a ‘real’ report, but photos & address Changed for privacy reasons – your information is 100% private)

[Historical Appraisal Sample – Click Here]

Contact

If you need a Step-Up in Basis or Date of Death appraisal, or if a professional advisor has requested one on your behalf, you may reach us here:

Click here to send us a message or call (408) 363-8924